According to the European Commission, over 65% of digital businesses selling across EU borders struggle with VAT compliance in their first two years of operation. What most official guides won’t tell you is that the One-Stop Shop (OSS) system, while designed to simplify VAT reporting, introduces hidden complexity that can cost businesses thousands in unexpected fees, penalties, and lost time. If you’re scaling cross-border sales in the EU, understanding the real-world mechanics of OSS isn’t optional—it’s the difference between smooth operations and compliance chaos.

The OSS registration process looks straightforward on paper, but businesses regularly face 6-8 week processing delays during peak periods, far exceeding the advertised 30-day timeline. This impacts cash flow planning for SaaS and e-commerce companies expecting quarterly filings to be quick and predictable. More critically, OSS doesn’t automatically handle all VAT liabilities—B2B exemptions still require manual tracking, creating overlooked compliance gaps that auditors actively target.

What OSS Actually Covers (And What It Doesn’t)

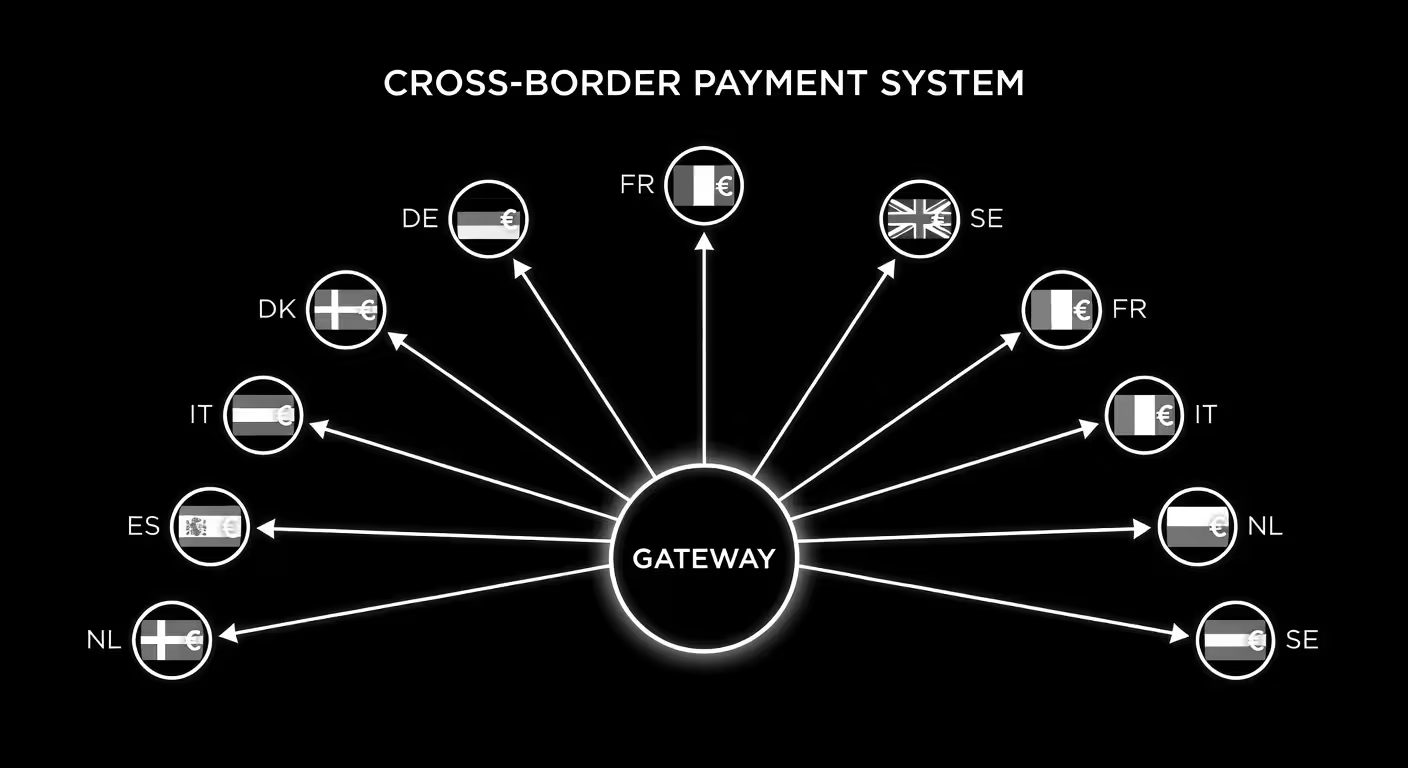

The OSS system allows businesses to report and pay VAT on cross-border B2C sales across all EU member states through a single quarterly return filed in their home country. This eliminates the need for separate VAT registrations in each country where you sell. However, the €10,000 annual threshold for OSS eligibility creates a trap: threshold calculations often ignore intra-EU supply chains, causing unexpected VAT hits when you scale beyond that limit.

What official documentation fails to emphasize is that OSS registration doesn’t replace the need to understand local tax nuances in your target markets. B2B transactions remain exempt from OSS reporting, but verifying customer status requires manual checks using tools like the VIES database. Failure to properly validate B2B exemptions is one of the most common triggers for audits, with fines averaging €2,000-€5,000 according to compliance specialists.

For digital services—software subscriptions, online courses, consulting—VAT rates vary from 17% to 27% across EU countries (Eurostat, 2024). OSS requires you to charge the customer’s local rate, which means dynamic pricing based on location. One growth hacker shared on X that their SaaS startup overpaid by 15% for six months due to incorrect country mappings in their payment system, a costly error that stemmed from assuming their payment gateway handled VAT automatically.

The Real Cost of OSS Compliance

While the EU promotes OSS as a cost-saving measure, insiders report annual accounting fees of €500-€2,000 just for verification and filing support. These costs aren’t mentioned in official portals. According to tax consultants working with digital businesses, quarterly filings consume 20-40 hours of internal time on data reconciliation alone, especially for companies with variable pricing models or multiple revenue streams.

The hidden work includes:

- Validating customer locations – IP addresses don’t always match billing addresses, creating rate application disputes

- Currency conversion tracking – OSS filings require EUR conversion, but exchange rate fluctuations add unreported volatility to liabilities

- Refund handling – OSS doesn’t retroactively adjust VAT for refunds, forcing manual claims that can take months and tie up cash

- Integration maintenance – Payment gateways like Stripe require custom API configurations to capture OSS data accurately, details their official documentation glosses over

One anonymous case highlighted by EU compliance forums involved a digital services company hit with a €50,000 fine for underreporting due to untracked B2C threshold crossings. The business had assumed their accounting software automatically flagged OSS obligations—it didn’t. This illustrates how theory diverges from reality: OSS works smoothly for low-volume operations but strains under scale without robust internal systems.

Post-Brexit Complications Nobody Warned You About

UK businesses selling into the EU now face a dual registration burden not highlighted in EU guidelines: both OSS for services and IOSS (Import One-Stop Shop) for goods. According to HMRC data, this has doubled administrative costs for UK-based e-commerce sellers targeting EU customers, with many abandoning certain markets due to complexity.

The practical impact includes:

- Maintaining separate VAT numbers for UK domestic, EU OSS, and potentially local registrations in high-volume countries

- Tracking which sales fall under which regime based on product type, customer location, and order value

- Currency exposure on both GBP-EUR conversions and EUR-based VAT liabilities

For SaaS companies, the service vs. goods distinction matters: software licenses typically fall under OSS, but if you ship physical products (like branded merchandise or hardware), IOSS becomes necessary for orders under €150. This split creates reporting complexity that most global SaaS businesses don’t anticipate when planning EU expansion.

Integration Challenges Payment Gateways Don’t Advertise

Most businesses assume Stripe, PayPal, or Paddle handle OSS reporting automatically. The reality is more complex. Payment gateways capture transaction data, but OSS filing requires specific data formatting and customer validation that standard integrations don’t provide out of the box.

CTOs on X debate the technical side extensively, with consensus that:

- Custom API configurations are needed to pull OSS-compliant data from Stripe—their standard VAT reports don’t match EU filing requirements

- Manual overrides are necessary for refunds and credits, which the automated flow doesn’t handle

- Rate limiting during quarterly filing periods can cause API failures if you’re batch-exporting large transaction volumes

One practical workaround shared by developers involves creating middleware that transforms payment gateway data into OSS-ready formats. This custom layer handles edge cases like partial refunds, currency conversions, and B2B exemption flags. Open-source GitHub repositories provide starting templates for WooCommerce and Shopify, filling gaps in official documentation.

For businesses handling thousands of transactions monthly, insiders recommend quarterly “dry runs” of OSS filings to catch discrepancies early. This practice has saved companies from penalties by identifying rate application errors or missing customer location data before submission deadlines.

When OSS Makes Sense vs. Local VAT Registration

The debate between OSS and local VAT registration isn’t clear-cut. For low-volume sellers (under €100,000 annual EU sales), OSS typically reduces administrative burden despite its quirks. But for high-volume operations, local registrations can actually cut costs long-term.

OSS Advantages

Single quarterly filing covering all EU countries. No need for local tax advisors in each market. Lower setup costs for businesses testing new markets. Simplified reporting through your home country tax portal.

Local Registration Benefits

Better cash flow through local VAT recovery on business expenses. Avoids OSS processing delays and manual reconciliation work. More control over audit processes. Can be more cost-effective above €200,000 annual sales per country.

Hybrid Approach

Many growing businesses use OSS for smaller markets while maintaining local VAT registration in their top 2-3 countries by revenue. This balances administrative simplicity with cost optimization and audit protection.

The decision often comes down to transaction volume and geographic concentration. If Germany represents 60% of your EU sales, a local German VAT number may save more than OSS simplifies. But if you’re selling evenly across 15+ countries with modest volumes in each, OSS remains the practical choice despite its operational friction.

Practical Tactics for Smoother OSS Operations

Professionals who’ve scaled through OSS share specific tactics that reduce friction:

Automate threshold monitoring. Tools like Avalara’s OSS connector track sales by country in real-time, flagging when you’re approaching the €10,000 limit. This prevents the common error of exceeding thresholds without triggering OSS registration, which can result in retroactive demands averaging €15,000 according to compliance case studies.

Implement IP geolocation with fallback. Dynamic VAT calculation based on customer IP reduces cart abandonment by 10-20% compared to static rate tables (Baymard Institute). But always include manual country selection as a fallback—IP databases have 5-10% error rates in border regions.

Use the VIES API for B2B validation. This free EU tool validates VAT numbers in real-time, reducing error rates in OSS reports by catching invalid B2B exemptions before they’re filed. Integration takes under an hour for most platforms.

Batch OSS data exports strategically. API rate limits during quarter-end filing periods can cause failures. Export transaction data incrementally throughout the quarter rather than pulling everything in the final week. This prevents the data bottleneck that causes rushed, error-prone filings.

Test with the EU’s OSS simulator. This lesser-known tool allows pre-filing tests that reveal edge cases like partial refunds or mixed B2B/B2C transactions. Running simulations quarterly catches formatting issues before submission deadlines.

For e-commerce businesses handling both physical and digital products, separating OSS (services) from IOSS (goods under €150) in your accounting system prevents the most common filing mistakes. Use distinct SKU prefixes or product categories that automatically route to the correct reporting stream.

Costly Mistakes That Trigger Audits

EU tax authorities actively monitor OSS filings for patterns that suggest non-compliance. Common triggers include:

Address validation failures. One e-commerce firm lost €8,000 in disputes over IP vs. billing address mismatches that led to incorrect rate applications. Their payment system used IP for VAT calculation but submitted billing country in OSS reports—auditors caught the discrepancy within two quarters.

Threshold calculation errors. Ignoring the €10,000 limit leads to retroactive VAT demands. Businesses have faced bills up to €15,000 for overlooked sales that crossed the threshold mid-year. The calculation must include ALL distance sales to EU consumers, not just digital services.

Refund handling gaps. OSS doesn’t retroactively adjust VAT for customer refunds. You must manually claim adjustments, which can take 3-6 months and tie up significant cash. Failing to track refunds separately from new sales creates reporting discrepancies that auditors flag immediately.

Business structure changes without OSS updates. Adding new product lines, changing business addresses, or restructuring entities requires OSS registration updates. Not updating within 30 days triggers automatic audits, with fines averaging €2,000-€5,000 even if no tax was underpaid.

Translation errors in non-English submissions. Some member states require OSS documentation in local languages. Over-relying on automated translation for German or French submissions has caused rejections that delay refunds by entire quarters. One case involved a mistranslated product category that resulted in a 12% rate differential and a €6,000 correction demand.

Principales sources citées

- OSS registration and compliance rules. European Commission, VAT e-commerce package (updated 2024). Commission européenne

- VAT rates across EU member states. Eurostat, VAT rates applied in the Member States of the European Union (2024 data). Eurostat

- B2B VAT exemption validation. European Commission, VIES VAT number validation system. VIES Database

- Impact of local payment methods on conversion. Baymard Institute, cart abandonment research (average 10-20% improvement with localized pricing). Institut Baymard

- Post-Brexit VAT complications for UK sellers. HMRC, VAT rules for goods and services sold to the EU. HMRC

Do I need OSS registration if I only sell to businesses (B2B)?

Do I need OSS registration if I only sell to businesses (B2B)?

No. OSS only covers B2C (business-to-consumer) sales. B2B transactions where you provide a valid VAT number use the reverse charge mechanism instead, where the customer accounts for VAT. However, you still need to validate those VAT numbers through VIES and maintain records to prove B2B status during audits.

What happens if I cross the €10,000 threshold mid-year?

What happens if I cross the €10,000 threshold mid-year?

You must register for OSS within 10 days of crossing the threshold and start charging destination-country VAT rates on all subsequent sales. You’ll need to file a correction for any sales after crossing the threshold where you charged your home country rate instead of the customer’s rate. Failure to register triggers retroactive demands that average €15,000 in practice.

Can I deduct VAT I paid on business expenses through OSS?

Can I deduct VAT I paid on business expenses through OSS?

No. OSS only covers VAT you collect from customers—it doesn’t allow input VAT recovery on expenses. For that, you need local VAT registration in the country where you incurred the expense. This is one reason high-volume sellers often choose local registration in their main markets despite OSS availability.

How do I handle refunds in OSS filings?

How do I handle refunds in OSS filings?

Refunds require manual adjustment in your OSS return for the quarter when the refund was issued, not the original sale quarter. You’ll report negative values in the appropriate country section. This doesn’t happen automatically—you need separate tracking systems for refunds to ensure accurate OSS data, otherwise you overpay VAT and must file separate claims that can take 3-6 months to process.

Does my payment gateway automatically handle OSS reporting?

Does my payment gateway automatically handle OSS reporting?

Not automatically in most cases. Stripe, PayPal, and similar platforms collect transaction data but don’t format it for direct OSS submission. You’ll need custom API configurations or middleware to transform payment data into OSS-compliant formats, handle B2B exemption flags, and manage refund adjustments. Standard VAT reports from payment gateways don’t match EU filing requirements without additional processing.